Summary

Indicator had been upgraded to Yellow caution from Orange Pre-crash level on April 22

Yen Volatility is reliable leading Indicator for global equities markets

Yen has biggest one day gain versus dollar since 2010 on April 28, 2016

The appreciation of the yen versus all of the world's currencies on April 28, 2016, has resulted in the NIRP Crash Indicator going from a Pre-Crash Orange reading to a Cautionary Yellow reading. The NIRP indicator going from Yellow to Orange increases the probability of a market crash being imminent.

The ranking system for the NIRP Crash Indicator’s signals are freely available and posted at www.dynastywealth.com daily, as follows:

Red: Full-Crash; Orange: Pre-Crash; Yellow: Caution; Green: All-Clear.

Information about origin, development and reliability of the NIRP Crash Indicator is also available at the Dynasty Wealth website.

Red: Full-Crash; Orange: Pre-Crash; Yellow: Caution; Green: All-Clear.

Information about origin, development and reliability of the NIRP Crash Indicator is also available at the Dynasty Wealth website.

The signal change was the result of the yen making significant gains against all of its major peer currencies on April 28, 2016. The yen’s three percent appreciation versus the dollar represented its largest increase for a single day since 2010. The sudden and significant appreciation of the yen was caused by the Bank of Japan (BOJ) announcing upon the conclusion of its April 28, 2016 meeting that it would not be increasing the utilization of monetary stimulus.

Currency exchange rate volatility between the yen and all of its major peer currencies has escalated to levels previously unseen. As recently as Friday, April 22, 2016, the NIRP Crash Indicator went from Orange, where it had been firmly entrenched since April 1, 2016 to Yellow, after having spent the entire month of March at Cautionary Yellow. See "No April Fool's Joke: NIRP Crash Indicator Elevated to Pre-Crash Warning".

After the NIRP Crash Indicator experienced extended periods of stability with only one signal change from the beginning of March through the first 22 days of April, the volatility of the indicator has increased considerably. The signal went from Orange to Yellow on Friday April 22 and back to Orange within six days on Thursday April 28. For more about this see my recent Seeking Alpha post.

Yen is a reliable leading indicator for global equities markets

Based on the 40 years of experience that I have in predicting the movements of markets, stocks and currencies, etc., and the research that I have conducted on prior crashes, including the Crash of 2008, my conclusion is that when volatility increases significantly for the yen it becomes a leading crash indicator. The Japanese yen and the U.S. dollar are the world's two largest single country reserve currencies. For this reason, the yen is the best default safe-haven currency utilized by investors during any U.S. and global economic and market crises. When crises unfold, historically the U.S. dollar — by far the world's most liquid and largest safe-haven currency — is susceptible to dramatic declines until the storm has passed.

Savvy investors know that the U.S. is, unquestionably, considered the world's leading economy and markets. They know that upon a crash of the U.S. stock market the initial knee-jerk reaction would be a simultaneous crash of the U.S. dollar versus the world's second leading single-nation currency. The yen is currently the default-hedge currency. Even though the euro, arguably, ranks with the U.S. dollar as the world's top reserve currency, it is not the preferred hedge against the greenback. The euro is shared by 19 of the European Union's member countries that have wide-ranging social and economic policies, and political persuasions. For this reason, and also because Japan is considered to be one of the most fiscally conservative countries on the planet, the default currency is the yen. The U.S. dollar does not experience extended crashes versus the Swiss franc and the British pound during times of crises because each of the underlying countries has economies much smaller than Japan's.

The currency and S&P 500 charts below depict the performance of the dollar yen exchange rate and its corresponding relationship to the performance of the S&P 500. The charts are for the 12 month and 10 year periods ended April 8, 2016. These charts were utilized for my conducting of the research and the charts were incorporated into my April 11, 2016, "Yen Volatility Is Leading Indicator For Market Sell-Offs" post. I highly recommend the viewing of the 7 minute 35 second video below "Yen Volatility Causes Market Crashes". It is a video interview of me by SCN’s Jane King about the subject matter of this specific report. I also explain all of the charts in this report during my interview.

The trajectory of the extended downward spikes of the U.S. dollar versus the yen in August of 2015, and from January 31, 2016 to February 11, 2016 coincide with the downward spikes that were made by the S&P 500 and Nikkei 225 over the same periods. (The S&P 500 and Nikkei 225 chart appears under the chart immediately below.)

The "S&P 500 vs. Nikkei 225" chart above depicts the price performance correlations between the two major world stock indices for the global stock market crashes that occurred in August of 2015 and January/February of 2016. The above chart also depicts the divergence, or anomaly that has occurred between the Nikkei 225 and the S&P 500 since the beginning of April 2016. Given the prior price crash correlations of the world's two major stock indices, which coincide with the crashes of the U.S. dollar as compared to the yen, the probability is high that the divergence, or anomaly will prove to be temporary.

The 10-year U.S. dollar and Japanese yen chart below explains the relationship between the U.S. dollar and the yen during the crash of global markets that began in 2008 prior to Lehman's declaring bankruptcy, and lasted into early 2009. The chart depicts the U.S. dollar's declined by approximately 20% from 110.55 yen to 87.28 yen during the four-month period, which began in August of 2008 and ended in December of 2008. The chart depicts an approximate 10% decline in the U.S. dollar as compared to the Japanese yen from February to April of 2016. The chart also depicts that the U.S. dollar as of April 8, 2016 has not yet bottomed. Further, should the decline be equivalent to the decline of 2008 the U.S. dollar would fall below 100 yen.

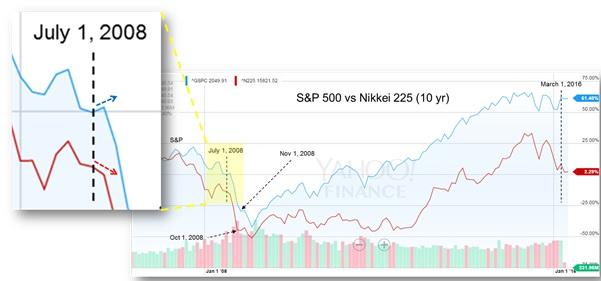

Below is a 10-year price-comparison chart for the S&P 500 and the Nikkei 225. At July 1, 2008 the charts for the Nikkei 225 and the S&P 500, which had been descending since May of 2008, diverged. The Nikkei 225 continued downward and the S&P went upward on July 1, 2008. The Nikkei continued on a downward spike trajectory until the index reached a base of support on October 1, 2008. The S&P 500 continued on its slightly upward trajectory until August 1, 2008. The S&P 500 than began a rapid descent, or spike, that resulted in its not finding its first base of support until November 1, 2008. Based on the 2008 charts, the Nikkei led the S&P 500 by a month during the crash of 2008. The chart also depicts the most recent divergence of the S&P 500 and Nikkei 225.

In Summary

Based on the body of research that I have conducted on spreading negative rates and the devastating effect that they are having on the global banking system, the probability is high that the major global stock indices (including the S&P 500) will begin a significant decline by 2018 at the latest. My April 11, 2016 article entitled, "Negative Rates Could Send S&P 500 To 925 If Not Eliminated," provides details about the potential mark down of the S&P 500 could likely be in stages. I highly recommend the viewing of my 9-minute 34-second video interview by SCN’s Jane King, entitled, "Why Negative Rates Could Send the S&P 500 to 925". In the video below I explain the math supporting the S&P 500’s decline to below 1000, and the reason it may be the only remedy to eliminate negative rates.

There are two reasons I am recommending the Short biased ETFs listed below: (i) the NIRP Crash Indicator going from Yellow to Orange has heightened the probability of a crash occurring; (ii) and, the three key central banks of the world — including the Bank of Japan (BOJ), European Central Bank (ECB), and the U.S. Federal Reserve — will not hold scheduled policy meetings until June of 2016. What that means is that the central banks cannot initiate any new monetary stimulus until June. The announcement by the BOJ on April 28, 2016 that it would not be adding any additional stimulus is bound to weigh on the markets until the next policy meetings are held by any of the key central banks. Since most of the appreciation of the markets since the crash of 2008 has been attributable to monetary and fiscal stimulus it is logical to conclude that the BOJ’s “do-nothing” decision will encourage profit taking during the month of May.

- ProShares Short S&P 500 ETF (NYSEARCA:SH)

- ProShares UltraPro Short Dow30 (NYSEARCA:SDOW)

- ProShares UltraPro Short S&P500 (NYSEARCA:SPXU)

- ProShares UltraPro Short QQQ (NASDAQ:SQQQ)

- ProShares UltraPro Short Russell2000 (NYSEARCA:SRTY)

- ProShares Short Dow 30 (NYSEARCA:DOG)

- ProShares UltraPro S&P 500 (NYSEARCA:UPRO)

- ProShares UltraShort Dow30 (NYSEARCA:DXD)

- ProShares UltraShort 20+ Year Treasury (NYSEARCA:TBT)

- ProShares UltraShort QQQ (NYSEARCA:QID)

- ProShares UltraShort S&P 500 (NYSEARCA:SDS)

Finally, the BOJ’s April 28, 2016 announcement reduces the probability of the market spiking to new highs in the near term. See “Bank of Japan Announcement Could Spike Market to New Highs”, April 27, 2016.

Below please find active links to all of my articles pertaining to negative rates:

- Japan's NIRP Increases Probability of Global Market Crash, March 4, 2016

- Negative Rates Could Send S&P 500 To 925 If Not Eliminated, April 11, 2016

- Negative Rates Pose Grave Risks To All Global and U.S. Banks, April 11, 2016

- Yen Volatility Is Leading Indicator For Market Sell-Offs. April 11, 2016

- Bank of Japan Announcement Could Spike Market to New Highs, April 27, 2016

For the record, throughout my 40-year career I have always been a bull investor and have never invested as a bear. Even with my concerns about the macro-market, I am very bullish on several public and private micro-cap opportunities, which have the potential to multiply by 10- to 100-times by 2020. My reports covering some of my recommendations are FREELY available at my Dynasty Wealth Investing community’s website.

{kind=link}

{kind=link}

{kind=link}

{kind=link}