Thursday, December 22, 2016

#INSURANCE: Lemonade Goes Nationwide—But Is It the Great Disru...

#INSURANCE: Lemonade Goes Nationwide—But Is It the Great Disru...: Lemonade Goes Nationwide—But Is It the Great Disruptor? " People need people who can explain complicated contracts and concepts. Insu...

Friday, November 4, 2016

Short Pick Noodles Misses

Last night after the close Noodles (NASDAQ: NDLS) reported a weak 3rd Quarter sending the stock down at the open this morning 5%.

Equities Research Summer Newsletter Short Picks are all down significantly over the 4 months since the picks were made, while the Standard and Poors 500 Index remains flat.

Under Armour Reported 3rd Quarter Financials last week sending stock down $7 for the week.

Next up will be Titan Machinery reporting 3rd Quarter financials either the last week of November or early December. Unlike Noodles and Under Armour, which are just over valued stocks with weakening fundamentals, Titan Machinery may find themselves out of business soon unless they are able to raise capital.

Warning on Titan Machinery

Thursday, November 3, 2016

Under Armour Stock Down 36%

Under Armour (NYSE: UA $30.79) closed yesterday down 36% since closing @ $48.20 (adjusted for split) on November 2,2015. Over the Same 1 year period the S&P500 Index which closed yesterday @ 2097 is down a mere 7 points from November 2,2015 close @ 2097 (is flat.)

The company filed their 3rd quarter 10Q with the Securities and Exchange Commission yesterday.

Highlights from 10Q

- DEBT INCREASES to Over $1 Billion

- Related Party Transactions : CEO Kevin Plank entity Sagamore Development Holdings sold property for $70.3 million to Under Armour. According this news story the sale price was more than twice what Plank paid for the property in 2014.

- Allowance for Doubtful Accounts As of 9/30/16 $33.6 million, 12/31/15 $5.9 million 9/30/15 $6.3 million.

- Under Armour trailing 9 qtrs (aggregate) Negative -($280 Million) operational cashflow. $1 Billion/debt

- Company Improved EPS growth due to lower Q3 2016 (32.6%) tax rate vs Q3 2015 (38.8%)

- Company enjoys higher gross profit margins because they record shipping and handling fees as net revenue but expense the cost as selling and general administrative expenses vs cost of revenue. The $25.7 million in Q3 charged in SG&A helped gross profit increase from 45.7% to 47.5%.

- Company Recorded more than $65 Million of Net Revenue from shipping and handling fees for the first 9 months of 2016 up from $40 million attributed to net sales in first nine months of 2015

Equities Research Warning on Monday October 24th, the day prior to the 3rd Quarter Earning press release.

Below is the performance of the October Put Options from Monday the 24th to Friday October 28th.

Put Prices on Friday October 28

Monday, October 24, 2016

Short Pick: Under Armour Hype Will Take Back Seat To Weak Fundamentals This Week

Under Armour (NYSE: UA) will report 3rd quarter financials on Tuesday and Wall Street continues to be Bullish.

Equities Research continues to Warn Investors to stay away from this high flyer and focus on the weak fundamentals and not the Hype! At end of day the rising debt, high interest expenses and declining operational cash flow will be reflected into a lower stock price.

Trade Card from Capital Market Laboratory

Performance of Recent Short Picks from EQUITIES RESEARCH

Equities Research continues to Warn Investors to stay away from this high flyer and focus on the weak fundamentals and not the Hype! At end of day the rising debt, high interest expenses and declining operational cash flow will be reflected into a lower stock price.

Trade Card from Capital Market Laboratory

UNDER ARMOUR WARNING MARCH 2016

Equities Research Short Pick Under Armour August 2007 Short @ $68. Shares slid to $15

Equities Research Short Pick Under Armour August 2007 Short @ $68. Shares slid to $15

Performance of Recent Short Picks from EQUITIES RESEARCH

- Titan Machinery : More Related Party Transactions

- Titan Machinery: Directors Draining All Cash In Related Party Deals

Saturday, October 15, 2016

Saturday, October 8, 2016

Friday, August 12, 2016

Summer 2016 Newsletter

(issued on July 1,2016 to paid subscribers)

Long Picks :

Symbid (SBID) $0.17 (Equity Crowdfunding)

MeetMe,Inc (MEET) $5.33

Sabre Corporation (SABR) $26.79

Short Picks

Under Armour (UA) $40.13

Titan Machinery (TITN) $ $11.15

Fundamental Charts

Disclaimer.

All Newsletters, published by Equities Research, LLC , does not constitute a recommendation by Equities Research, LLC to buy, sell, hold any security, or to follow any particular trading or investment strategy. Also, the information provided should not be construed as an offer, or a solicitation of an offer, to buy or sell securities. An investor's best course of action must be based upon individual circumstances. EquitiesResearch.com shall not be liable for any damages or costs of any type arising out of or in any way connected with your use of The Newsletters, or any of our services. EquitiesResearch.com, its officers and employees may buy and sell any position in the securities or companies mentioned |

| Content copyright 2010-2016. Equities Research LLC. All rights reserved |

Friday, July 1, 2016

Newsletter Pick Up 31%

Equities Research Newsletter pick Hershey UP 31% vs 1.7% gain for the S&P500.

Equities Research July 1, 2015 Newsletter featured a STRONG BUY on HERSHEY @ $86.53 (dividend adjusted).

Hershey closed yesterday @ $113.49, for a gain of $27 in exactly 1 year.

The Standard and Poors 500 index over the same 12 month period rose from 2063.11 to 2098.86 for a gain of 36 points.

Today, Readers should subscribe to Equities Research July 2016 Newsletter available NOW.

I've given plenty of great research in 27 years. My July 2016 pick is best risk/reward that I've ever found.

Order here and forward this to your friends.

SUBSCRIBE FOR JULY

Regards,

TOMMY

HAPPY 4TH OF JULY EVERYONE

about founder Tom Renna

Equities Research Monthly

Newsletter

Disclaimer. All Newsletters, published by Equities Research, LLC , does not constitute a recommendation by Equities Research, LLC to buy, sell, hold any security, or to follow any particular trading or investment strategy. Also, the information provided should not be construed as an offer, or a solicitation of an offer, to buy or sell securities. An investor's best course of action must be based upon individual circumstances. EquitiesResearch.com shall not be liable for any damages or costs of any type arising out of or in any way connected with your use of The Newsletters, or any of our services. All readers and subscribers and customers should consult a licensed financial advisor. EquitiesResearch.com, its officers and employees may buy and sell any position in the securities or companies mentioned. Content copyright 2010-2016. Equities Research LLC. All rights reserved

Equities Research July 1, 2015 Newsletter featured a STRONG BUY on HERSHEY @ $86.53 (dividend adjusted).

Hershey closed yesterday @ $113.49, for a gain of $27 in exactly 1 year.

The Standard and Poors 500 index over the same 12 month period rose from 2063.11 to 2098.86 for a gain of 36 points.

Today, Readers should subscribe to Equities Research July 2016 Newsletter available NOW.

I've given plenty of great research in 27 years. My July 2016 pick is best risk/reward that I've ever found.

Order here and forward this to your friends.

SUBSCRIBE FOR JULY

Regards,

TOMMY

HAPPY 4TH OF JULY EVERYONE

about founder Tom Renna

Contact Tom Renna (908) 477-4796 or thomasrenna@gmail.com

(3 Picks,Tickers Only) $250/month

($2500 for monthly newsletters w annual subscription

prepaid)

Research

Equities Research (Institutional Services)

Call 908-477-4796 or email thomasrenna@gmail.com

Disclaimer. All Newsletters, published by Equities Research, LLC , does not constitute a recommendation by Equities Research, LLC to buy, sell, hold any security, or to follow any particular trading or investment strategy. Also, the information provided should not be construed as an offer, or a solicitation of an offer, to buy or sell securities. An investor's best course of action must be based upon individual circumstances. EquitiesResearch.com shall not be liable for any damages or costs of any type arising out of or in any way connected with your use of The Newsletters, or any of our services. All readers and subscribers and customers should consult a licensed financial advisor. EquitiesResearch.com, its officers and employees may buy and sell any position in the securities or companies mentioned. Content copyright 2010-2016. Equities Research LLC. All rights reserved

Thursday, June 30, 2016

End of Quarter: Time to Paint the Tape

June 30th is End of Quarter. Mutual Funds and Money Managers are Notorious for MARKING up Stocks, aka Painting the Tape, to increase the asset value of their Equity Positions into the Month end. It is based on tonight's closing prices that many money managers get their fees (percentage of money under management).

So, this afternoon is a great time to Sell into the Inflated Prices and to even Short stocks, especially with the 3 day holiday weekend approaching.

#EquitiesResearch: ORDER Equities Research Newsletter & Research

#EquitiesResearch: ORDER Equities Research Newsletter & Research

Monday, May 16, 2016

$100 Invested in Uber in 2010 Would Be Worth Over $1 Million By 2015

One hundred dollars ($100) invested into Uber’s October 2010 private placement was valued at $1,050,000 by the end of 2015. The only problem is that it was not possible to invest an amount as small as $100 into Uber in 2010 due to a ban that the SEC had implemented in 1933. I highly recommend the video at the very bottom of this article. It provides details on how Uber became successful and how to find the next Uber.

With the SEC’s lifting of the crowdfunding ban today (May 16, 2016) every US citizen will be able to invest $100 or less into new companies for the first time since 1933. I highly recommend the video at the very bottom of this article. It provides details on how Uber became success and how to find the next Uber.

Prior to 1850 there was no such thing as an investor in the United States of America. Investing began because of the invention of the steam engine and the subsequent advent of railroads. Before the beginning of private investing, individuals merely deposited their money in banks. When banks refused to provide expansion capital to railroads, it became a motivating factor for pioneer merchants and residents to withdraw their money from the banks and become first-time investors in railroad stocks and bonds to encourage prosperity for their communities. The 6 minute 43 second video below covers how crowdfunding evolved in the 1840s, why the SEC banned it in 1933, and the future of crowdfunding because of the SEC’s lifting of the second and final ban on May 16, 2016.

There was no such thing as an investment bank or stock broker in the U.S. at the time individual investing began. Those whom the public trusted to make their first-ever investments and to ensure that their monies were being utilized to build the railroad were the community’s merchants and businessmen. One such merchant was Henry Lehman. He immigrated to Montgomery, Alabama in 1844 and set up a cotton exchange. The outcome of the success that Lehman and his brothers had in getting railroads financed was their founding of the Lehman Brothers investment bank in 1850, six years after Henry Lehman had immigrated to America. Goldman Sachs and the other investment banks, which were founded in the last half of the 1800s, all had deeply imbedded railroad roots. These new investment banks and their pioneer investors who financed the railroads went on to finance the companies that emerged to transform the economy from agricultural to industrial from the 1880s to the 1920s.

Major Inventions & Industrial CompaniesGenerating Dynasty Wealth Founded 1885-1919

| ||

Invention/Company

|

Co. and Year Founded

|

Market Cap 11/20/15

|

Telephone

|

AT&T (T), 1885

|

$207B

|

Electricity

|

General Electric (GE), 1889

|

$310B

|

Automobile

|

Ford Motor (F), 1903

|

$58B

|

Computer

|

IBM (IBM), 1911

|

$134B

|

Airplane

|

Boeing (BA), 1916

|

$100B

|

Radio

|

RCA, 1919

|

N/A acquired by GE

|

For a community, having railroad service was crucial to its very survival. Likewise, the laying of vast networks of railroad tracks from 1860 to 1890 is analogous to the advent of the Internet, which resulted in the majority of the world’s population gaining access to the World Wide Web and e-mail service in the late 1990s.

The railroad transformed the U.S. economy from being agrarian-based to having an industrial base. The railroads and then the Internet, which began the transformation of the U.S. economy from industrial to digital, are definitely the two greatest economic developments that have occurred within the U.S. during each of the last two centuries.

The birth of investing culminated with securities fraud becoming rampant in the 1920s, a period that became infamous as the “roaring twenties”. Growing fraud and corruption culminated both in the Stock Market Crash of 1929 and the ensuing nationwide Great Depression.

Four years after the Great Depression began, the United States Securities & Exchange Commission (SEC) was established. The SEC immediately implemented two laws prohibiting businesses (i) from advertising to raise capital, and (ii) from raising capital from individuals who were not accredited investors (possessing a minimum net worth of $1 million). The SEC also implemented rules and regulations requiring a business to utilize a licensed broker-dealer.

The complex network, or ecosystem, established by the SEC in 1933 and 1934, for the purpose of motivating investors to trust the securities markets, provided the capital for new inventions and businesses until 2010, when the Dodd Frank Act was passed and became law. Dodd Frank was a response to the crash of 2008, and it significantly increased the liability for the broker-dealers that financed new inventions and emerging companies. The Act also increased the SEC’s enforcement powers and increased its ability to prosecute broker-dealers. This resulted in many broker-dealers ceasing to finance new inventions and companies. The ecosystem that had been in place since 1933 was broken.

In 2012, the JOBS Act was passed. Under its provisions the SEC was mandated by the U.S. Congress to lift both of the bans that the SEC had put into place in 1933. In September of 2013, the SEC lifted the advertising ban. On May 16, 2016, the SEC lifted the ban prohibiting non-accredited individuals from investing in early-stage and start-up companies.

There were two caveats for the SEC’s lifting the ban. The first was that all entities wishing to raise capital from a crowd of non-accredited investors utilize a SEC approved funding platform. The second caveat was that a funding platform not promote or recommend any entity seeking funds over any other entity seeking funds. The limiting of a funding platform’s ability to promote or recommend a business needing funding created the need for Social Investing communities.

My October 20, 2014 “Crowdfunding Must Get Back to Its Roots” article explains why social investing communities would have to emerge for crowdfunding to be successful. Researching the history of investing and the ensuing in-depth studies of crowdfunding led to the founding of the Dynasty Wealth Investing Community in April of 2014. It also led to my conceiving of the Trophy Investing community.

Since Trophy will specialize in educating the crowd and will cull from all of the crowdfunding opportunities to recommend only the very best ones to community members I predict that it will become the Facebook of social or community investing. To become a member of the Trophy Investing community go to www.michaelmarkowsk.net and sign up for a FREE 30 day trial subscription to the Trophy Investing letter. The letter recommends the shares of micro-cap companies that have the potential to multiply in price within 5 years and the plan is to also recommend crowdfunding opportunities.

With the SEC’s lifting of its crowdfunding bans that had been in place since 1933 and the founding of Dynasty Wealth and the three other social investing communities mentioned in my October 2014 article, social or community investing is now back to its 1850 roots. The social investing communities will once again rise to be the primary financier of the companies that will drive the growth of the world economy.

Dynasty Wealth LLC, the “boutique” research firm that I founded evolved from research that I had conducted on the ongoing transformation from the industrial economy to the digital economy. My findings enabled me to conclude that the period from 2015 through 2020 would be the best ever for investors to generate dynasty wealth returns of 10- to 100-times from utilizing a truly diversified portfolio. The video entitled, “Digital disruptor companies have the potential to get $10 billion valuations quickly,” below provides details about how investing into a portfolio of digital disruptors enable investors to create dynasty wealth. It discusses digital disruptor UBER. A $10,000 investment into UBER in 2010 was valued for $105 million in 2015. I recently discovered a digital disruptor in the $593 billion U.S. grocery industry and my research recommendation covering it is available at www.michaelmarkowski.net.

Friday, April 29, 2016

NIRP Crash Indicator back to Pre-Crash Level

Michael Markowski |

Summary

Indicator had been upgraded to Yellow caution from Orange Pre-crash level on April 22

Yen Volatility is reliable leading Indicator for global equities markets

Yen has biggest one day gain versus dollar since 2010 on April 28, 2016

The appreciation of the yen versus all of the world's currencies on April 28, 2016, has resulted in the NIRP Crash Indicator going from a Pre-Crash Orange reading to a Cautionary Yellow reading. The NIRP indicator going from Yellow to Orange increases the probability of a market crash being imminent.

The ranking system for the NIRP Crash Indicator’s signals are freely available and posted at www.dynastywealth.com daily, as follows:

Red: Full-Crash; Orange: Pre-Crash; Yellow: Caution; Green: All-Clear.

Information about origin, development and reliability of the NIRP Crash Indicator is also available at the Dynasty Wealth website.

Red: Full-Crash; Orange: Pre-Crash; Yellow: Caution; Green: All-Clear.

Information about origin, development and reliability of the NIRP Crash Indicator is also available at the Dynasty Wealth website.

The signal change was the result of the yen making significant gains against all of its major peer currencies on April 28, 2016. The yen’s three percent appreciation versus the dollar represented its largest increase for a single day since 2010. The sudden and significant appreciation of the yen was caused by the Bank of Japan (BOJ) announcing upon the conclusion of its April 28, 2016 meeting that it would not be increasing the utilization of monetary stimulus.

Currency exchange rate volatility between the yen and all of its major peer currencies has escalated to levels previously unseen. As recently as Friday, April 22, 2016, the NIRP Crash Indicator went from Orange, where it had been firmly entrenched since April 1, 2016 to Yellow, after having spent the entire month of March at Cautionary Yellow. See "No April Fool's Joke: NIRP Crash Indicator Elevated to Pre-Crash Warning".

After the NIRP Crash Indicator experienced extended periods of stability with only one signal change from the beginning of March through the first 22 days of April, the volatility of the indicator has increased considerably. The signal went from Orange to Yellow on Friday April 22 and back to Orange within six days on Thursday April 28. For more about this see my recent Seeking Alpha post.

Yen is a reliable leading indicator for global equities markets

Based on the 40 years of experience that I have in predicting the movements of markets, stocks and currencies, etc., and the research that I have conducted on prior crashes, including the Crash of 2008, my conclusion is that when volatility increases significantly for the yen it becomes a leading crash indicator. The Japanese yen and the U.S. dollar are the world's two largest single country reserve currencies. For this reason, the yen is the best default safe-haven currency utilized by investors during any U.S. and global economic and market crises. When crises unfold, historically the U.S. dollar — by far the world's most liquid and largest safe-haven currency — is susceptible to dramatic declines until the storm has passed.

Savvy investors know that the U.S. is, unquestionably, considered the world's leading economy and markets. They know that upon a crash of the U.S. stock market the initial knee-jerk reaction would be a simultaneous crash of the U.S. dollar versus the world's second leading single-nation currency. The yen is currently the default-hedge currency. Even though the euro, arguably, ranks with the U.S. dollar as the world's top reserve currency, it is not the preferred hedge against the greenback. The euro is shared by 19 of the European Union's member countries that have wide-ranging social and economic policies, and political persuasions. For this reason, and also because Japan is considered to be one of the most fiscally conservative countries on the planet, the default currency is the yen. The U.S. dollar does not experience extended crashes versus the Swiss franc and the British pound during times of crises because each of the underlying countries has economies much smaller than Japan's.

The currency and S&P 500 charts below depict the performance of the dollar yen exchange rate and its corresponding relationship to the performance of the S&P 500. The charts are for the 12 month and 10 year periods ended April 8, 2016. These charts were utilized for my conducting of the research and the charts were incorporated into my April 11, 2016, "Yen Volatility Is Leading Indicator For Market Sell-Offs" post. I highly recommend the viewing of the 7 minute 35 second video below "Yen Volatility Causes Market Crashes". It is a video interview of me by SCN’s Jane King about the subject matter of this specific report. I also explain all of the charts in this report during my interview.

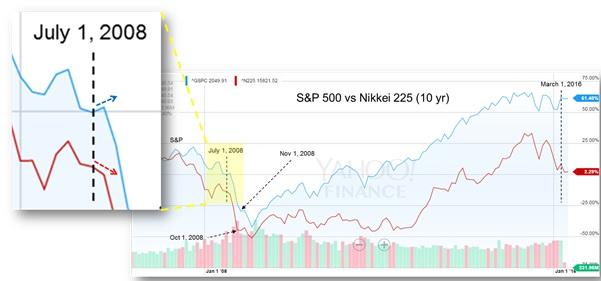

The trajectory of the extended downward spikes of the U.S. dollar versus the yen in August of 2015, and from January 31, 2016 to February 11, 2016 coincide with the downward spikes that were made by the S&P 500 and Nikkei 225 over the same periods. (The S&P 500 and Nikkei 225 chart appears under the chart immediately below.)

The "S&P 500 vs. Nikkei 225" chart above depicts the price performance correlations between the two major world stock indices for the global stock market crashes that occurred in August of 2015 and January/February of 2016. The above chart also depicts the divergence, or anomaly that has occurred between the Nikkei 225 and the S&P 500 since the beginning of April 2016. Given the prior price crash correlations of the world's two major stock indices, which coincide with the crashes of the U.S. dollar as compared to the yen, the probability is high that the divergence, or anomaly will prove to be temporary.

The 10-year U.S. dollar and Japanese yen chart below explains the relationship between the U.S. dollar and the yen during the crash of global markets that began in 2008 prior to Lehman's declaring bankruptcy, and lasted into early 2009. The chart depicts the U.S. dollar's declined by approximately 20% from 110.55 yen to 87.28 yen during the four-month period, which began in August of 2008 and ended in December of 2008. The chart depicts an approximate 10% decline in the U.S. dollar as compared to the Japanese yen from February to April of 2016. The chart also depicts that the U.S. dollar as of April 8, 2016 has not yet bottomed. Further, should the decline be equivalent to the decline of 2008 the U.S. dollar would fall below 100 yen.

Below is a 10-year price-comparison chart for the S&P 500 and the Nikkei 225. At July 1, 2008 the charts for the Nikkei 225 and the S&P 500, which had been descending since May of 2008, diverged. The Nikkei 225 continued downward and the S&P went upward on July 1, 2008. The Nikkei continued on a downward spike trajectory until the index reached a base of support on October 1, 2008. The S&P 500 continued on its slightly upward trajectory until August 1, 2008. The S&P 500 than began a rapid descent, or spike, that resulted in its not finding its first base of support until November 1, 2008. Based on the 2008 charts, the Nikkei led the S&P 500 by a month during the crash of 2008. The chart also depicts the most recent divergence of the S&P 500 and Nikkei 225.

In Summary

Based on the body of research that I have conducted on spreading negative rates and the devastating effect that they are having on the global banking system, the probability is high that the major global stock indices (including the S&P 500) will begin a significant decline by 2018 at the latest. My April 11, 2016 article entitled, "Negative Rates Could Send S&P 500 To 925 If Not Eliminated," provides details about the potential mark down of the S&P 500 could likely be in stages. I highly recommend the viewing of my 9-minute 34-second video interview by SCN’s Jane King, entitled, "Why Negative Rates Could Send the S&P 500 to 925". In the video below I explain the math supporting the S&P 500’s decline to below 1000, and the reason it may be the only remedy to eliminate negative rates.

There are two reasons I am recommending the Short biased ETFs listed below: (i) the NIRP Crash Indicator going from Yellow to Orange has heightened the probability of a crash occurring; (ii) and, the three key central banks of the world — including the Bank of Japan (BOJ), European Central Bank (ECB), and the U.S. Federal Reserve — will not hold scheduled policy meetings until June of 2016. What that means is that the central banks cannot initiate any new monetary stimulus until June. The announcement by the BOJ on April 28, 2016 that it would not be adding any additional stimulus is bound to weigh on the markets until the next policy meetings are held by any of the key central banks. Since most of the appreciation of the markets since the crash of 2008 has been attributable to monetary and fiscal stimulus it is logical to conclude that the BOJ’s “do-nothing” decision will encourage profit taking during the month of May.

- ProShares Short S&P 500 ETF (NYSEARCA:SH)

- ProShares UltraPro Short Dow30 (NYSEARCA:SDOW)

- ProShares UltraPro Short S&P500 (NYSEARCA:SPXU)

- ProShares UltraPro Short QQQ (NASDAQ:SQQQ)

- ProShares UltraPro Short Russell2000 (NYSEARCA:SRTY)

- ProShares Short Dow 30 (NYSEARCA:DOG)

- ProShares UltraPro S&P 500 (NYSEARCA:UPRO)

- ProShares UltraShort Dow30 (NYSEARCA:DXD)

- ProShares UltraShort 20+ Year Treasury (NYSEARCA:TBT)

- ProShares UltraShort QQQ (NYSEARCA:QID)

- ProShares UltraShort S&P 500 (NYSEARCA:SDS)

Finally, the BOJ’s April 28, 2016 announcement reduces the probability of the market spiking to new highs in the near term. See “Bank of Japan Announcement Could Spike Market to New Highs”, April 27, 2016.

Below please find active links to all of my articles pertaining to negative rates:

- Japan's NIRP Increases Probability of Global Market Crash, March 4, 2016

- Negative Rates Could Send S&P 500 To 925 If Not Eliminated, April 11, 2016

- Negative Rates Pose Grave Risks To All Global and U.S. Banks, April 11, 2016

- Yen Volatility Is Leading Indicator For Market Sell-Offs. April 11, 2016

- Bank of Japan Announcement Could Spike Market to New Highs, April 27, 2016

For the record, throughout my 40-year career I have always been a bull investor and have never invested as a bear. Even with my concerns about the macro-market, I am very bullish on several public and private micro-cap opportunities, which have the potential to multiply by 10- to 100-times by 2020. My reports covering some of my recommendations are FREELY available at my Dynasty Wealth Investing community’s website.

Wednesday, April 27, 2016

Related Party Transactions Appear to Be Slippery

(4 of 8 directors that sat on Board from last May 2015 have now resigned according to latest 10K, including the founder of company who also quit as the president without any explanation, No new president has been named since he quit as president in June 2015.)

TITN stock has sky rocketed UP 62% from $8 on February 11th to $12.93 in 10 weeks. A Penny Stock Brokerage Firm out of Minnesota , FELTL,has said after the company reported over a (-$30 Million) Loss for the 2nd consecutive FY that the stock could "easily" go to $40 as reported by Dow Jones on the morning of March 18th when shares had one of top volume days of the year. IN November FELTL estimated that TITAN would have net income of $20 Million in FY2017, Titan said on CC that they would NOT be profitable in FY17.

Normally a Definitive proxy filing would be a run of the mill cookie cutter disclosure naming directors and small proposals up for a vote that are usually insignificant, but not when it involves Titan Machinery!

Equities Research first raised a red flag on the issuer based on poor fundamentals, specifically a pattern of Cashless Earnings with significant amounts of negative operational cash flow. A further examination learned that the company was no more than a roll up story consisting of mom and pop retailers that the company was financing through the issuance of debt and more debt. But it wasn't until the company filed a PROXY Statement in April of 2013 that it was discovered this company was being financially raped by management's related party transactions.

Today we won't discuss the DEF 14 filed in April 2013 that the Securities and Exchange Commission Division of Corporate Finance spent 8 months exchanging comment letters on with the company.

Today we won't discuss the Proxy Proposal that was voted down by the Shareholders in June 2013.

Today we won't discuss the DEF 14 filed in 2015 when the Company asked for shareholders to give their proxy vote to the President of the company only to have the President suddenly resign from the company (3 days after the filing) without updating the DEF14. (Company has still not disclosed why the founder resigned from the board, stepped down as president and left the company. The company has not had a president since June 2015. Severance Agreement has been disclosed.)

OWNER (& Spouse) of a Titan Machinery Related Party, Charged with 29 FELONY TAX CRIMES

In 2012 the Minnesota Department of Revenue Charged the owner of C.I. Construction with 21 felonytax crimes.

Since the charge, C.I. Construction has generated revenue of $13 million directly from Titan Machinery. (prior to the charge we are to believe that C.I. Construction did not do any business with Titan)

MAY 2013 Titan Machinery for the First time Included C.I. Construction as a Related Party

Its peculiar that C.I. Construction was not disclosed as Related Party prior to 2013 considering Titan Machinery grew from 2 stores to 100 stores over that time span.

Here is A Video from YouTube that CI CONSTRUCTION advertises for the work they did for Titan Machinery in FY2012. But there was NEVER ANY DISCLOSURE OF THIS RELATED PARTY DEAL IN SEC FILING FY2012.

Fact is C I Construction was a related party with Titan prior to FY2013 but there was no disclosure.

http://articles.aberdeennews.com/2011-10-21/farmforum/30308885_1_titan-machinery-case-ih-storage-building

Today we will shed light on the RELATED PARTY TRANSACTION that the company discloses with a construction company which is also a reseller of the company's products.

The company discloses in their filings that the contractor, C.I. Construction, owner is a brother in law of two brothers that founded TITAN MACHINERY and sit on the board. (one brother is the president who recently resigned and the other who also is the investment banker to Titan still sits on the board.)

C I Construction is disclosed in SEC filings as a RELATED PARTY because the Owner, Rob Thompson, is the (3) brother in law of the two founders (directors) and the Treasurer of the company.

C.I.CONSTRUCTION (RELATED PARTY) Received the following Payouts:

FY2013: $6.7 Million

FY2014: $3.9 Million

FY2015: $1.9 Million

FY2016: $0.5 Million

total 4 years: $13 Million

In the past year C.I. advertises on their website they are building 2 of the biggest projects in the history of Titan and its peculiar that they ONLY earned $500K in FY2016? hmmm

Ted Christensen is the treasurer of Titan Machinery but is also listed as an officer of C.I.Construction.

TITAN Disclosure (Ted Christianson is our Treasurer and Vice President, Finance. He joined Titan in 2003 and is responsible in his senior financial role to secure access to capital both domestically and internationally as well as managing overall financial risk.)

Ted Christensen is also listed as an officer of Dealer Sites, LLC which is also disclosed as a RELATED PARTY of TITAN MACHINERY. DEALER SITES is an entity that many of the Management of TITAN have an EQUITY INTEREST (Christensen family members and the Chairman of TITAN, David Meyer.) Dealer Sites has recently disclosed it has increased contracts with DEALER SITES from under $50 Million to over $100 Million.

IT GETS MORE BIZZARE. IS C.I.Construction and Dealer Sites one in the same? According to this TAX document , YES. And this GOVERNMENT Document too. C.I CONSTRUCTION shares the Same Address of DEALER SITES on certain other Documents with Ted Christensen as the contact person.

Another RELATED PARTY DISCLOSURE in Titan Machinery Disclosure is C.I. FARM POWER refers to a company owned by company's founder , Peter Christensen who recently Suddenly stepped down as a Board Member and resigned from company.

THERE is no disclosure whether C.I.FARM POWER is related to C.I. Construction. I am assuming that C.I. in the Farm Power company and the C.I. Construction are both created from Christensen Incorporated.

In 2011 when Peter Christensen disclosed in his sale of 200,000 shares of stock @ $27.80 the position that he sold was shares of C.I. Farm Power.

According to this Article: C.I. stands for Christenson Incorporated and is owned by ROB THOMPSON and PETER CHRISTENSON. But there is NO DISCLOSURE in SEC Filings pertaining to Thompson owning CI Farm Power nor Christenson owning CI CONSTRUCTION.

2016 Construction Management Services Performed by C.I. Construction, LLC

C.I. Construction, LLC ("CI"), performs construction management services for certain of the Company's new store construction projects, shop additions, and remodel projects. CI is owned by Rob Thompson, who is the brother-in-law of Peter Christianson (our former President and former member of our Board of Directors) and of Tony Christianson (a member of our Board of Directors). CI performs construction management services including developing designs/specifications and drawings, preparing bid packages, advising on the selection of suppliers and contractors, and overseeing the construction process. CI is also an authorized reseller of certain steel buildings that the Company frequently incorporates into its construction projects.

CI receives a fee equal to 4.5% of the construction costs, excluding expenditures for certain fixtures and fixed assets that the Company originates. CI is also reimbursed for the labor costs of CI's site supervisors and on-site staff, and utilities, equipment rental, travel, and other direct costs incurred by CI in performing the services. CI also receives payment as a reseller of the steel buildings used in certain of our construction projects. We are not obligated to retain CI on an ongoing basis, and this decision will be made for each project based on the best interests of the Company. During fiscal 2016, CI received an aggregate amount of $474,717 in direct or indirect payments from the Company for the performance of construction-related services and the purchase of steel buildings, as well as reimbursement for other construction-related costs.

Today we won't discuss the DEF 14 filed in April 2013 that the Securities and Exchange Commission Division of Corporate Finance spent 8 months exchanging comment letters on with the company.

Today we won't discuss the Proxy Proposal that was voted down by the Shareholders in June 2013.

Today we won't discuss the DEF 14 filed in 2015 when the Company asked for shareholders to give their proxy vote to the President of the company only to have the President suddenly resign from the company (3 days after the filing) without updating the DEF14. (Company has still not disclosed why the founder resigned from the board, stepped down as president and left the company. The company has not had a president since June 2015. Severance Agreement has been disclosed.)

OWNER (& Spouse) of a Titan Machinery Related Party, Charged with 29 FELONY TAX CRIMES

In 2012 the Minnesota Department of Revenue Charged the owner of C.I. Construction with 21 felonytax crimes.

Since the charge, C.I. Construction has generated revenue of $13 million directly from Titan Machinery. (prior to the charge we are to believe that C.I. Construction did not do any business with Titan)

MAY 2013 Titan Machinery for the First time Included C.I. Construction as a Related Party

Its peculiar that C.I. Construction was not disclosed as Related Party prior to 2013 considering Titan Machinery grew from 2 stores to 100 stores over that time span.

Here is A Video from YouTube that CI CONSTRUCTION advertises for the work they did for Titan Machinery in FY2012. But there was NEVER ANY DISCLOSURE OF THIS RELATED PARTY DEAL IN SEC FILING FY2012.

Fact is C I Construction was a related party with Titan prior to FY2013 but there was no disclosure.

http://articles.aberdeennews.com/2011-10-21/farmforum/30308885_1_titan-machinery-case-ih-storage-building

Today we will shed light on the RELATED PARTY TRANSACTION that the company discloses with a construction company which is also a reseller of the company's products.

The company discloses in their filings that the contractor, C.I. Construction, owner is a brother in law of two brothers that founded TITAN MACHINERY and sit on the board. (one brother is the president who recently resigned and the other who also is the investment banker to Titan still sits on the board.)

C I Construction is disclosed in SEC filings as a RELATED PARTY because the Owner, Rob Thompson, is the (3) brother in law of the two founders (directors) and the Treasurer of the company.

C.I.CONSTRUCTION (RELATED PARTY) Received the following Payouts:

FY2013: $6.7 Million

FY2014: $3.9 Million

FY2015: $1.9 Million

FY2016: $0.5 Million

total 4 years: $13 Million

In the past year C.I. advertises on their website they are building 2 of the biggest projects in the history of Titan and its peculiar that they ONLY earned $500K in FY2016? hmmm

Ted Christensen is the treasurer of Titan Machinery but is also listed as an officer of C.I.Construction.

TITAN Disclosure (Ted Christianson is our Treasurer and Vice President, Finance. He joined Titan in 2003 and is responsible in his senior financial role to secure access to capital both domestically and internationally as well as managing overall financial risk.)

Ted Christensen is also listed as an officer of Dealer Sites, LLC which is also disclosed as a RELATED PARTY of TITAN MACHINERY. DEALER SITES is an entity that many of the Management of TITAN have an EQUITY INTEREST (Christensen family members and the Chairman of TITAN, David Meyer.) Dealer Sites has recently disclosed it has increased contracts with DEALER SITES from under $50 Million to over $100 Million.

IT GETS MORE BIZZARE. IS C.I.Construction and Dealer Sites one in the same? According to this TAX document , YES. And this GOVERNMENT Document too. C.I CONSTRUCTION shares the Same Address of DEALER SITES on certain other Documents with Ted Christensen as the contact person.

Another RELATED PARTY DISCLOSURE in Titan Machinery Disclosure is C.I. FARM POWER refers to a company owned by company's founder , Peter Christensen who recently Suddenly stepped down as a Board Member and resigned from company.

THERE is no disclosure whether C.I.FARM POWER is related to C.I. Construction. I am assuming that C.I. in the Farm Power company and the C.I. Construction are both created from Christensen Incorporated.

In 2011 when Peter Christensen disclosed in his sale of 200,000 shares of stock @ $27.80 the position that he sold was shares of C.I. Farm Power.

According to this Article: C.I. stands for Christenson Incorporated and is owned by ROB THOMPSON and PETER CHRISTENSON. But there is NO DISCLOSURE in SEC Filings pertaining to Thompson owning CI Farm Power nor Christenson owning CI CONSTRUCTION.

- "Earl Christianson became the sole owner of Christianson’s Inc. and, Earl’s son Peter and son-in-law Rob Thompson are assuming leadership positions in what has become a three-generation family business"

2016 Construction Management Services Performed by C.I. Construction, LLC

C.I. Construction, LLC ("CI"), performs construction management services for certain of the Company's new store construction projects, shop additions, and remodel projects. CI is owned by Rob Thompson, who is the brother-in-law of Peter Christianson (our former President and former member of our Board of Directors) and of Tony Christianson (a member of our Board of Directors). CI performs construction management services including developing designs/specifications and drawings, preparing bid packages, advising on the selection of suppliers and contractors, and overseeing the construction process. CI is also an authorized reseller of certain steel buildings that the Company frequently incorporates into its construction projects.

CI receives a fee equal to 4.5% of the construction costs, excluding expenditures for certain fixtures and fixed assets that the Company originates. CI is also reimbursed for the labor costs of CI's site supervisors and on-site staff, and utilities, equipment rental, travel, and other direct costs incurred by CI in performing the services. CI also receives payment as a reseller of the steel buildings used in certain of our construction projects. We are not obligated to retain CI on an ongoing basis, and this decision will be made for each project based on the best interests of the Company. During fiscal 2016, CI received an aggregate amount of $474,717 in direct or indirect payments from the Company for the performance of construction-related services and the purchase of steel buildings, as well as reimbursement for other construction-related costs.

2015 Construction Management Services Performed by C.I. Construction, LLC

C.I. Construction, LLC, ("CI") performs construction management services for certain of the Company's new store construction projects, shop additions, and remodel projects. CI is owned by Rob Thompson, who is the brother-in-law of Tony Christianson (a member of our Board of Directors) and Peter Christianson (a member of our Board of Directors and our President). CI performs construction management services including developing designs/specifications and drawings, preparing bid pack ages, advising on the selection of suppliers and contractors, and overseeing the construction process. CI is also an authorized reseller of certain steel buildings that the Company frequently incorporates into its construction projects.

CI receives a fee equal to 4.5% of the construction costs, excluding expenditures for certain fixtures and fixed assets that the Company originates. CI is also reimbursed for the labor costs of CI's site supervisors and on-site staff, and utilities, equipment rental, travel, and other direct costs incurred by CI in performing the services. CI also receives payment as a reseller of the steel buildings used in certain of our construction projects. We are not obligated to retain CI on an ongoing basis, and this decision is made for each project based on the best interests of the Company. At times, we have utilized a competitive bidding process for construction management services.

During fiscal 2014, CI received an aggregate amount of $3.9 million in direct or indirect payments from the Company for the performance of construction-related services and the purchase of steel buildings, as well as reimbursement for other construction-related costs. We do not believe the terms of any of the transactions and agreements described above are any less favorable to us than could be obtained in an arm's length transaction with an unrelated party.

CI CONSTRUCTION PROJECTS

- INFLATED ASSETS AND UNDERSTATED LOSSES

- INSIDER SELLING

- INSIDER TRADING BEFORE NEWS

- RELATED PARTY TRANSACTIONS

- SEC COMMENT LETTERS

- Auditor Sudden Resignation

- RELATED PARTY TRANSACTIONS

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Subscribe to:

Posts (Atom)