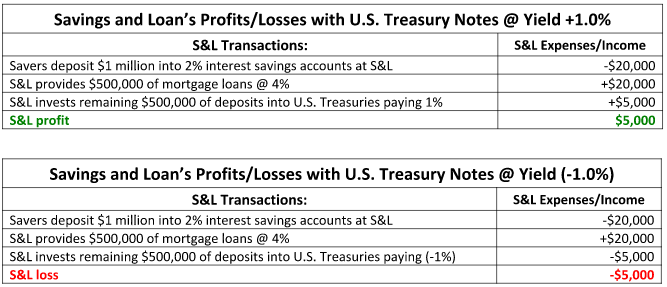

Should the yields of U.S. Treasury debt securities become negative a meltdown of the global banking system and a crash of the global markets might be inevitable. Based on my analysis the only solution, other than the central banks taking action, to rid the world of the

insidious NIRPs and negative interest rates would be that all of the world’s income-producing assets undergo significant markdowns. See my March 12, 2016 “

Negative Rates Pose Grave Risks to Banks” report.

Since the beginning of 2016, I observed a degree of volatility that I had only seen in 2008. Given my many years of experience and track record for developing algorithms, which enabled me to

warn investors about pending calamities — including

Lehman, Bear Stearns and Merrill Lynch in 2007 — I conducted extensive research on the crash of 2008. I discovered metrics that could have been used to predict the 2008 crash, and the V-shaped reversal. These metrics are components for an algorithm that is now powering my “NIRP Crash Indicator”, which can signal an impending market crash. The NIRP Crash Indicator signals are free and are posted daily at

www.dynastywealth.com. See March 9, 2016 “

New Indicator to Predict Market Crashes” article.

The best solution to stop the spreading of NIRPs and negative interest rates is for central banks of the world to immediately enact or redact policies to abolish them. This would be the catalyst for the yields of the sovereign securities of Japan and Germany becoming positive. In the absence of this happening, a possible remedy to fight the NIRP and negative interest rate contagion could be the resetting of valuations of all income-producing assets to a discount in the marketplace as compared to their most recent valuations. The decline in valuations of income-producing assets would result in a significant increase in their yields. The yields increasing to sufficient levels should motivate safe haven and other investors to liquidate their holdings in negative- and low-yielding sovereign debt securities to purchase the less secure and much higher-yielding income-producing assets. The availability of significantly higher yields on income-producing assets would, hopefully, discourage safe haven and other savvy investors from “being fearful”, and encourage them to “become greedy”.

With significant declines in the values of all less secured income-producing assets, and resultant increase in their yields, market forces would take over. The result would be that markets would drive down prices of treasuries and other sovereign debt securities, and their yields upward into substantial positive territory. Upon yields of the world’s sovereign debt securities skyrocketing, the demand for and prices of negative and low interest rate securities will collapse. The need for central banks to utilize NIRPs will have been completely exhausted.

Case Study: American Electric Power versus 10-Year U.S. Treasury Note

To prove my theory and validate my suggested remedy, I conducted research on the share price and dividend yield behavior of the public utility company, American Electric Power (NYSE: AEP), before and after the crash of 2008. I also focused my research on the price action and yields of 10-Year U.S. Treasury bonds over the same period. My focus was on a utility company because shares of a utility have always been considered the safest form of equity investments. If a utility bill is not paid the electricity is turned off. For this reason a utility’s dividend payments are reliable. Thus, the dividends of a utility company are much more secure than are dividends of any non-utility company. During the Great Depression AEP was able to maintain and increase cash dividends. For these reasons it is assumed that the yield for shares owned of a utility will always be lower than the yield that they might expect to receive from shares they hold of a dividend-paying non-utility company.

The shares of American Electric Power (AEP) is a good example of a safe income-producing asset that could potentially motivate a holder of negative or extremely low interest rate sovereign securities to liquidate them to purchase its shares. With a current annual dividend of $2.24, and a most recent share price of $62.00, AEP has a yield of 3.63%. Based on how AEP’s yield and share price behaved before and after the crash of 2008, an increase of its yield to 10% would likely be sufficient to motivate a holder of a low or negative interest rate sovereign securities to buy its shares. A decline in AEP shares by approximately $40, or by 64% to a share price of $22 would increase its dividend yield to 10%. Should such a scenario unfold it would be very similar to what happened to AEP’s share price and yield before and after the crash of 2008.

On July 31, 2008 AEP’s share price was $27.84, and its annual dividend yield was 5.9%. From the end of July 2008 to March 9, 2009 — the same date that the S&P 500 Index (the Index) bottomed — AEP’s share price declined by almost $10 (or by 36%) to a 5-year low of $17.73 and to an equivalent

dividend yield of 9.2%. Over the same period the price of a 10-year U.S. Treasury note increased by 33%, and the yield fell from 4% to 3%. In June of 2009, three months after AEP’s share price had bottomed, the price of AEP shares had increased by 21% and its yield had fallen to 7.6%. Over the same three months the price of the 10-year Treasury bond declined by 25% and its yield had gone back to the 4% from which it started a year earlier. Based on the opposite behavior of yields, the price action of AEP shares, and the 10-year Treasury notes from July of 2008, through June of 2009, it is very likely that holders of the notes were selling them to purchase shares of AEP and other high-yielding utility companies. See CNBC’s

historical yields chart for 10-Year U.S. Treasury notes. My research confirms that holders of Treasuries and sovereign debt securities will sell them for less secure income-paying securities upon the yields increasing substantially.

On March 10, 2016 the dividend yield for the S&P 500 — based on its close at a value of 1989 — was 2.2%. Under the assumption that the dividend yield of the Index would have to be at 10% to become attractive to safe-haven and savvy investors, the Index would have to decline to 430, based on the current annual $43.00 dividend. While such a correction of approximately 80% would be severe, it would not likely be the Index’s low. A crash or correction of such magnitude would likely cause the first global depression since the 1930s. After the Index’s dividend hit an all-time high in 1930, the dividend declined by 44% by 1935 and did not eclipse the 1930 high until 1955.

There is voluminous empirical data covering the price and yield action of utility shares and sovereign debt securities, before and after the 2008 crash. For this reason it would be difficult to fathom any argument that theS&P 500 would not have to go to a yield of at least 10% to dislodge safe-haven investors from their holdings of U.S. Treasury notes and other sovereign debt securities.

Assuming that all of the world’s central banks that have instituted NIRPs do not repeal them, the issue would become how the resets of the world’s income-producing equity and non-sovereign debt markets — required to exterminate the NIRPs and negative interest rates — might take form? Will it be a swift crash, or a gradual correction? My hunch is that the correction could occur with valuations of the markets ratcheting downward in stages. Markets would not likely bottom until late 2017, or early 2018 for two reasons, as follows:

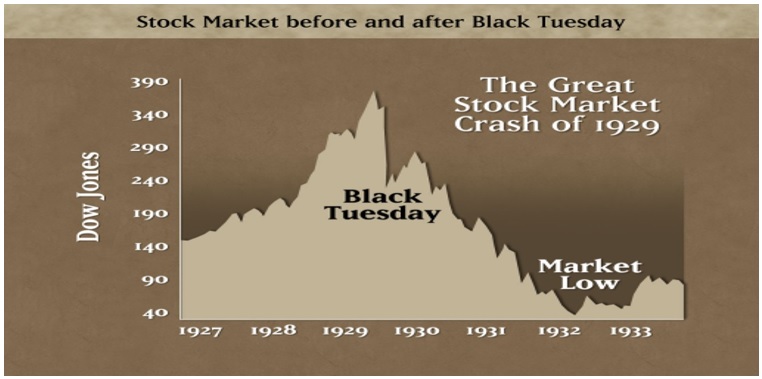

- A correction of more than 40% from a market’s all-time high to its trough has historically taken time. There have been five such corrections over the last 100 years, as follows: 1919 to 1921, 1929 to 1932, 1973 to 1974, 2000 to 2002, and 2007 to 2009. (The four corrections, prior to the one ending in 2009, lasted at least 24 months.) Had massive fiscal and monetary stimulus not been applied in October of 2008, after Lehman filed for bankruptcy, this most recent correction would likely have lasted at least 24 months.

- If the dividend yield of the S&P 500 Index should go from a most recent 2% to 10% to kill the NIRPs and negative interest rates, the peak-to-trough decline of the Index would be 80%. The only other time over the last 100 years in the U.S. that a decline of more than 50% occurred was from 1929 through 1932. After the market had declined by an initial 40% in October of 1929, the market experienced six powerful rallies that generated trough-to-peak rallies providing returns ranging from 20% to 50%. When the market finally bottomed in the middle of 1932 it had declined by 90% from its 1929 all-time high. Since history has been known to repeat itself I would expect no less drama from the secular bear market that was likely birthed after the market hit an all-time high in May of 2015.

The only remaining issue is the timing of when the S&P 500 Index might begin to ratchet downward to new multi-year lows that could eventually take the Index to well below 1000 by late 2017 or early 2018. Extreme controversy surrounding the NIRPs and negative interest rates has continued to escalate since the Bank of Japan (BOJ) instituted a NIRP earlier in 2016. It has also increased the probability of the Index’s descent happening sooner rather than later. For this reason it is likely that the news pertaining to NIRPs will be the catalyst that causes the beginning of the next market downturn. Because NIRPs were created by the world’s central banks the next downturn to lower lows will likely be fueled by public statements that will be made by central bankers about NIRPs, negative rates, stimulus, and the health of economies, etc.

A perfect example of this occurred on March 10, 2016, as I watched the European Central Bank’s (ECB’s) press conference pertaining to changes to its interest policies implemented at the conclusion of the regularly scheduled policy meeting on same date. The four most significant revelations from the ECB press conference and my brief comments follow:

- Interest rates and inflation projected to remain low in Europe through 2019

Onset of deflation risk to remain high

- ECB to buy investment-grade corporate bonds

- Lower profits resulting from NIRP, offset by capital gains on banks’ bond holdings

Capital gains are non-recurring

- NIRPs do not work for all bank business models

Confirms NIRPs are now creating dysfunction for banking system

An in-depth report is underway that will provide explanations regarding the consequences each item the ECB revealed above will have on the world’s markets. One of my conclusions is obvious: the flight into safe-haven sovereign debt securities will accelerate. My March 12, 2016 report entitled, “Negative Rates Pose Grave Risks to Banks” also provides color on the ECB’s recent policy meeting, sovereign debt securities and save havens.

Fireworks could go off when the Fed concludes its scheduled March Policy Meeting on March 16, as there is no doubt that Fed Chair, Janet Yellen, will have to answer questions from Congressional leaders and the media about negative interest rates. Should Yellen give any indication that negative interest rates might be an option it could set off a chain of events that could result in negative- and/or low-interest rates becoming the headline campaign issue for the 2016 elections. I recently watched a video interview of David Stockman, former Budget Director under President Reagan. Based on what Stockman said about Donald Trump, the probability is high that the Presidential candidate will use Yellen’s statements to make negative- and/or low-interest rates his flagship campaign issue. There are millions of retired Democrats and Republicans with whom this issue would resonate. Since the 2008 debacle, passbook savings rates have been miniscule. Negative interest rates and deflation becoming the topic of discussion at dinner tables could, in itself, be the catalyst that produces a market meltdown or a recession. Please see the March 14, 2016 video:

“The Fed Is Lost: David Stockman”.

In the event that Fed Chair, Yellen, does not slip up on March 16, there will be plenty of additional central-banker sound bite opportunities throughout 2016. From April through December of 2016 each of the world’s three leading central banks have six scheduled policy meetings. What will most likely occur is that the S&P 500 and the indices for the other global markets will hit new multi-year lows during some or all of the months the meetings are scheduled.

Schedule of Remaining Policy Meetings of Central Banks for 2016

|

European Central Bank (ECB)

|

Bank of Japan (BOJ)

|

U.S. Federal Reserve (FOMC)

|

March 10, 2016

|

March 15, 2016

|

March 16, 2016

|

April 21, 2016

|

April 28, 2016

|

April 27, 2016

|

June 2, 2016

|

June 16, 2016

|

June 16, 2016

|

July 21, 2016

|

July 29, 2016

|

July 27, 2016

|

September 8, 2016

|

September 21, 2016

|

September 21, 2016

|

October 20, 2016

|

November 1, 2016

|

November 2, 2016

|

December 8, 2016

|

December 20, 2016

|

December 14, 2016

|

It is unlikely that the ECB and the BOJ will make the policy changes that would be needed to eliminate negative interest rates. The ECB in its March meeting announced that it had increased its NIRP from -0.03 to -0.04 the negative meeting The markets for the sovereign debt securities of Japan and Germany have already priced yields into negative territory. While its questionable that the U.S. Federal Reserve would institute a NIRP, the U.S. Central Bank is severely conflicted and compromised. After raising the discount rate in December of 2015 interest rates of the U.S. Treasury markets promptly declined. With the global economy having deteriorated and Japan having instituted a NIRP, the rational for the Fed to raise rates is fast evaporating. Even if the U.S. economy should weaken, the Federal Reserve would have to give serious consideration before lowering the discount rate. The markets would likely interpret a rate cut vs. a rate hike as a signal that the Fed would be moving in the direction of instituting a NIRP. The Fed’s being “conflicted” is yet another reason the markets are highly susceptible to a significant haircut by the end of 2016.

The writing herein is in further support of my February 26, 2016 foundational report “

Japan’s NIRP Increases Global Market-Crash Probability”, which is about NIRPs and deflation, and the potential devastating impact that both can have on corporate profits and on the markets. The report concluded that instituting of a NIRP (Negative Interest Rate Policy) by the Bank of Japan (BOJ) had significantly increased market volatility to a point that has increased the probability of a market crash. (My recommended investment strategy, which protects an investor’s capital against significant market corrections and crashes, is contained in an excerpt from my foundational report as follows:

“Pre-Crash ‘Black Swan’ Investing Strategy”.)

My foundational report also provides details on research that I had conducted on the Crash of 2008, which enabled me to discover the metrics that could have been used to predict the 2008 crash, and the V-shaped reversal. These metrics are now powering an indicator, or warning system, which I developed and named the “NIRP Crash Indicator”. It is currently being utilized to monitor the markets for indications of any impending crash and its freely available at

www.dynastywealth.com.

{kind=link}